Compare credit cards by use

Spend conditions apply.

Get 50,000 Bonus Membership Rewards Points

Highlights

- Obtain 50,000 Bonus Membership Rewards Points upon application approval and spending $4,000 on your new Card within the initial 3 months. T&Cs apply. Exclusive to New Amex Card Members.

- Enjoy a $400 Travel Credit annually for flights, hotels, and car rentals when booked online using this card.

- Benefit from complimentary domestic and international travel insurance coverage.

Pros

Cons

Transfer debt to a 0% credit card.

0% balance transfer cards

On website

Highlights

- Annual fee waived.

- 0% p.a. interest for 28 months on transferred balances (with a 3% balance transfer fee). Returns to 14.99% p.a. thereafter.

- No charges for foreign transactions.

- Offer valid for new customers within a specified timeframe. Additional fees and terms and conditions apply.

Pros

Cons

On website

Highlights

- Experience 0% p.a. interest on balance transfers for 12 months (with a 2% BT fee, then 12.99% p.a.).

- 0% p.a. for 12 months on purchases (reverting to 12.99% p.a.).

- Benefit from up to 55 interest-free days.

- Offer exclusively for new customers within a specified period. Additional charges, along with terms and conditions, apply.

Pros

Cons

On website

Citi Clear Credit Card

Highlights

- Benefit from 0% p.a. for 28 months on Balance Transfers (with a 2% Balance Transfer fee). Rate reverts to cash advance rate.

- Enjoy a low ongoing variable purchase rate of 14.99% p.a.

- Add up to 4 supplementary cardholders at zero additional expense.

Pros

Cons

Turn everyday spend into points.

Frequent flyer cards

Highlights

- No annual fee in the initial year, saving you $195.

- Accrue 3 Membership Rewards points for every $1 spent at major supermarkets and petrol stations.

- Access $200 allocated for annual travel expenses, applicable towards eligible flights, hotels, or car rentals when booked through American Express Travel.

Pros

Cons

Highlights

- Obtain 50,000 Bonus Membership Rewards Points upon application approval and spending $4,000 on your new Card within the initial 3 months. T&Cs apply. Exclusive to New Amex Card Members.

- Enjoy a $400 Travel Credit annually for flights, hotels, and car rentals when booked online using this card.

- Benefit from complimentary domestic and international travel insurance coverage.

Pros

Cons

On website

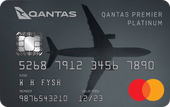

Highlights

- Get up to 100,000 bonus Qantas Points. Get 70,000 bonus Qantas Points upon spending $3,000 or more on eligible purchases within 3 months from card approval. Plus, an extra 30,000 bonus points if you haven't earned Qantas Points with a credit card in the past 12 months. Terms and Conditions apply.

- Benefit from 0% on Balance Transfer for 12 months with no Balance Transfer fee. Returns to Cash Advance rate thereafter. No interest-free days are applicable on retail purchases with an outstanding balance transfer.

- Benefit from the reduced annual fee of $349 p.a. for the initial year. An ongoing annual fee of $399 p.a. is applicable in the 2nd year.

Pros

Cons

Get a card with no annual fee.

No annual fee cards

Highlights

- Benefit from a competitive 10.99% p.a. interest rate for purchases.

- Enjoy a perpetual $0 annual fee with card ownership.

- Access up to 55 days interest-free.

Pros

Cons

Highlights

- Acquire Velocity Points while benefiting from a $0 annual card fee.

- Points accrued on your card seamlessly transfer to your Velocity account monthly and are redeemable for various rewards such as flights, lodging, car rentals, gift cards, and beyond.

- Earn 0.75 Velocity Points per $1 spent, except for transactions with Australian government entities, where you'll earn 0.5 Velocity Points per $1 spent.

Pros

Cons

On website

Citi Simplicity Card

Highlights

- No late fee. No annual fee.

- Benefit from 0% interest on Purchases for 6 months. Returns to ongoing Purchase rate afterward.

- Transfer your current balance at 0% for 6 months with a 0% balance transfer fee.

- Obtain extra cards with a $0 annual fee (up to 4 additional cardholders aged at least 16 years).

Pros

Cons

Helping Australians compare credit cards since 2008

1. Compare

Our well-established partnerships with providers allow us to offer you excellent value through a wide selection of deals and cards.*

2. Choose

Review offers, compare credit cards, and options from our selection of card issuers* and narrow down your choices based on your needs.

3. Save

Compare our range of issuers and card types* to determine if you can find a more suitable card.

What's the best credit card type for you?

Banks and alternative financial institutions in Australia offer numerous credit card types. Here are the types of credit card available.

Credit card comparison made simple

David Boyd, co-founder of Credit Card Compare, explains, "With hundreds of credit cards on the market offering a dizzying array of rates, fees and features, finding the right product for your spending habits and financial situation is challenging. Here at Credit Card Compare, we want to make it easier to cut through these complexities and provide Aussie consumers and businesses with a credit card comparison service to find their next credit card.”

What is a credit card?

A credit card represents a banking instrument that offers a pre-approved credit limit by a financial institution, enabling expenditures and bill payments. Issuers typically provide it in dual formats: a tangible card for physical transaction needs and a virtual version for seamless online usage.

How credit cards work

Credit cards work on a principle of borrowed financial capacity from a bank. A credit card facilitates the acquisition of goods and services like fuel, foodstuff, and utility settlements, positioning itself as a viable substitute to direct cash or savings through a bank card.

Credit cards are issued with specific spending caps, tailored by individual eligibility and vary across different offers and financial entities. Borrowers must settle expended credits, with accruing interest applied to any residual amount monthly.

How to compare credit cards and their features

When assessing credit cards, consider not just the card types, like Rewards versus Low Fee cards, but also their inherent characteristics*. Below is a concise enumeration of essential features for comparison:

- Purchase (interest) rate: The interest rate applied to your card's remaining balance after each billing cycle. Rewards cards often have higher rates than low fee cards.

- Honeymoon (or introductory) interest rate: Choosing a card offering '0% interest' usually means no interest for a predetermined timeframe. It's wise to verify the subsequent interest rate after this period.

- Interest-free days: It refers to the period when no interest is charged on purchases. Typically, these days are fixed within your billing cycle, not starting at the time of purchase.

- Fees, which may include: Annual or monthly fees, fees for participating in rewards programs, fees for late payments, cash advance fees, overdraft fees, and charges for international card use

- Minimum credit limit: The minimum credit offered by a bank or lender. Minimum limits vary by card, ranging from $500 to $6,000, based on the card, the issuer, and your eligibility.

- Rewards program: Certain cards feature rewards programs like AMEX, Velocity Frequent Flyer or Qantas Frequent Flyer rewards. Choose a card whose rewards scheme benefits you.

- Points rates: For rewards cards, this indicates the points earned per dollar spent

- Bonus points: Some rewards cards offer sign-up bonus points, redeemable for retail vouchers.

How to manage a credit card responsibly

One of the main problems with credit cards is that it's possible to get into debt that's hard to get out of without concerted effort, but there are practical steps to avoid this and use a credit card responsibly.

- Pay in full: Whenever possible, make payments in full each cycle before interest accrues. Consider lower-limit cards to encourage manageable spending.

- Avoid compounding debt: Start with reasonable initial limits. Temporarily switching to debit transactions can provide a needed spending reset.

- Seek help if needed: Reputable charities like the National Debt Helpline offer anonymous assistance in creating workable budgets and discussing card obligations.

- Talk with your lender: Issuers may permit structured payment plans allowing large yet navigable debt to be repaid over a more appropriate timeframe. It's best to contact them early.

Expert's opinion on whether a credit card is worth it

Andrew Boyd, co-founder of Credit Card Compare, explains, "Don't rush into it if you are unsure whether you need a credit card. Take time before making an informed decision."

"Credit cards require financial diligence but, when managed responsibly, can unlock useful benefits from rewards points to consumer protections. However, borrowing beyond your means can risk credit rating damage and spiralling debt." Before deciding, here are some questions to ask yourself.

- Do I have the discipline necessary? It's easy to overspend when you have credit available on a card.

- Can I pay off the balance in full each billing cycle? Interest-accruing balances can start to pile up.

- Am I financially stable enough? If your income is in doubt, a credit card is probably best avoided.

Who we are

Credit Card Compare is Australia's dedicated credit card comparison platform. Founded in 2008, our mission is to help Aussies compare credit cards and make informed decisions on their next credit card.